Addtime:2026-04-06 Hits:17

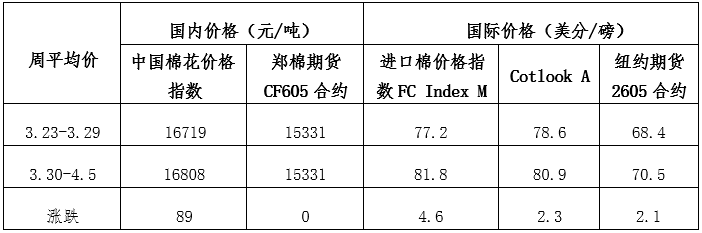

Last week (March 30–April 5), domestic spot cotton supplies remained ample. With the peak season for the cotton textile market already halfway through, downstream demand softened compared to the previous period; new orders were predominantly short-term, fragmented, and small-scale. Market participants expressed concern that April's consumption might have been "front-loaded" (prematurely exhausted), leading enterprises to limit their raw material procurement primarily to immediate replenishment needs. On the other hand, however, strong expectations of tighter supplies in the coming year—driven by intensified efforts to reduce cotton acreage in Xinjiang—combined with rising cultivation costs due to conflicts in the Middle East, provided significant support for cotton prices. Consequently, prices fluctuated within a narrow range at high levels throughout the week. The previous week (March 23–29) saw the cotton textile market in its traditional peak season, with new orders stimulating increased demand for raw material replenishment; however, as domestic cotton prices remained near their annual highs, corporate procurement behaviors remained cautious. Furthermore, price volatility in crude oil—which rippled through the chemical fiber and cotton supply chains—heightened cost-side uncertainties for enterprises, further influencing the pace of procurement.

During the same period, international cotton prices strengthened significantly. At the beginning of the week, U.S. cotton planting intentions exceeded expectations, creating short-term downward pressure on prices. Subsequently, however, a confluence of bullish factors—including intensifying drought in major production regions (fueling expectations of reduced yields), a sharp surge in U.S. cotton export commitments, skyrocketing international oil prices, and a weakening U.S. dollar—drove cotton prices upward. As a result, the price gap between domestic and international markets continued to narrow slightly.

The weekly average price of the China Cotton Price Index (CCIndex 3128B) stood at 16,808 yuan/ton, an increase of 89 yuan/ton from the previous week. The weekly average price of the Cotlook A Index (converted to RMB under a 1% tariff rate)—including a 200 yuan/ton port handling fee—was 13,771 yuan/ton. This figure was 3,037 yuan lower than the China Cotton Price Index (CCIndex 3128B), representing a narrowing of the price gap by 248 yuan compared to the previous week.

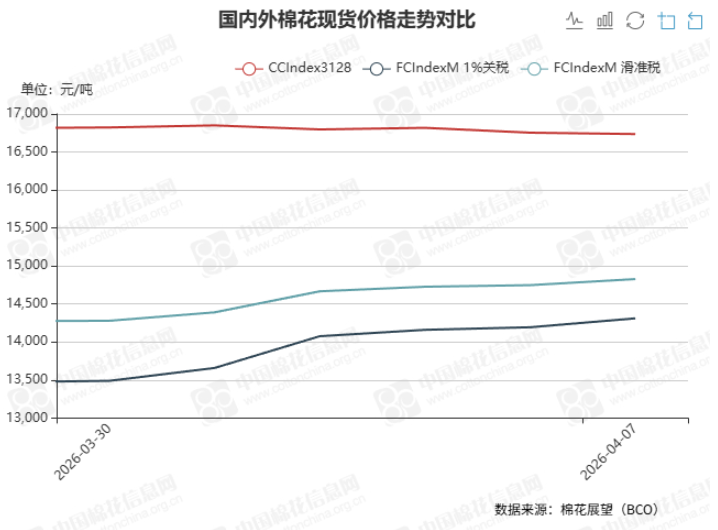

Cotton Price Trends

II. Xinjiang Cotton Spring Sowing Begins Earlier Than Usual

Since late March, most cotton-growing regions in Xinjiang have experienced higher-than-average temperatures and increased sunshine, creating meteorological conditions generally favorable for cotton sowing. In southern Xinjiang—specifically the Aksu and Kashgar prefectures—cotton sowing has commenced in succession, beginning earlier than is typical for this time of year. Temperatures across most of Xinjiang are expected to run higher than average during early April, creating favorable meteorological conditions for spring cotton sowing. Cotton-growing regions are advised to seize this window of favorable weather to sow at an opportune moment. Furthermore, they should remain attentive to weather alerts and take precautionary measures against sudden strong winds and temperature drops, thereby minimizing the potential for damage—such as torn plastic mulches and frost-damaged cotton seeds—caused by such adverse weather events.